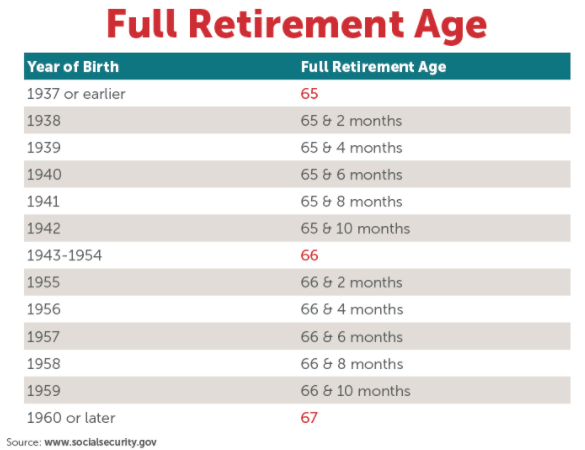

To maximize your Social Security benefits, it is important to know your options at 70. Know the limitations on claiming benefits and the reduction of the widow's rate at full-retirement age. Also, know about the options for suspending or claiming delayed retirement credit. Although there are no reasons to delay retirement to receive more money, there are certain strategies you can use.

Social Security benefits are not available to everyone.

Social security benefits for those over 70 are based upon the 35 years of highest earning employment adjusted for inflation. If your employment history is less than 35 years, your benefits may be lower than you anticipated. If you want to maximize your benefits, you may want to keep working beyond this age. Be aware, however, that your income will go up in taxes as well as Medicare premiums.

There are many ways to increase your monthly Social Security benefits. This can be done by waiting until 70 to apply for benefits. A program is available to married couples through the Social Security Administration. The recipient can file a restricted claim to spousal benefits if one spouse was born after 1954. This will allow them half of the FRA of the spouse they are claiming. However, they can continue building their own retirement benefits up to age 70 to switch to a larger benefit.

Impact of a reduced widow rate at full retirement

An increased widow's benefit at full retirement age might result in a decreased benefit for the survivor. The worker who died before the survivor can claim the benefit is the basis for the reduced rate. The reduced rate will be higher for younger workers.

While social security is intended to assist widows and their dependents in their transition, the lower rate will have an impact on their benefits. Additionally, the earnings test lowers the benefit amount. You will need to calculate your benefits on the basis of your FRA.

You have options to receive full retirement benefits

It is possible to suspend your social security benefits when you reach full retirement age. There are many options for those who have to temporarily suspend benefits. The voluntary suspension option allows you to suspend your benefits temporarily without the need to pay back.

You can delay the start of benefits by selecting voluntary suspension. This will result in delayed retirement credits which can be used to allow you later to begin receiving benefits. You can resume receiving benefits if you wait until you are 70 years old. You won't be required to repay any benefits you received during the suspension period. Your benefit will also increase by 8.5% per annum. You can also choose to suspend your benefits while you work.

You have options to claim delayed retirement credit

Social Security beneficiaries aged 70 and over can take the delayed retirement credit. This program allows individuals to continue working while still receiving benefits if they qualify. The program is designed to provide a larger monthly benefit for people over age 70 than they would have at 62. However, there are several factors to consider before deciding to claim this credit. There are also tax implications and investment opportunities.

The benefits of the delayed retirement credit are added to your monthly benefit in January of the calendar year you turn 70. If you are still employed, however, your delayed pension credits will not be added as an additional benefit to your monthly benefits. The benefit amount will only increase by a certain amount in January of the following year.

Premature retirement credit: limitations

There are limits to how early you can begin taking your Social Security benefits. If you are under 70, you must have worked for 35 years before you are able to start receiving your benefits. Your credit for delayed retirement can be used to delay your claim until you turn 70. The credit will increase your monthly benefit by eight per cent each year. Many people can get credit worth thousands of dollars each year.

There are two possible options for FRA: one that increases your retirement age to 68 years and the other to 70 years. The Social Security Administration (SSA) developed solvency estimates for both options. MINT is a microsimulation method that estimates the distributional impacts of these policies. The model was not intended to assume future changes in retirement behavior like a change in health or age.

FAQ

How does Wealth Management work?

Wealth Management is a process where you work with a professional who helps you set goals, allocate resources, and monitor progress towards achieving them.

Wealth managers can help you reach your goals and plan for the future so that you are not caught off guard by unanticipated events.

They can also prevent costly mistakes.

What are the various types of investments that can be used for wealth building?

There are several different kinds of investments available to build wealth. These are just a few examples.

-

Stocks & Bonds

-

Mutual Funds

-

Real Estate

-

Gold

-

Other Assets

Each has its own advantages and disadvantages. Stocks or bonds are relatively easy to understand and control. However, they can fluctuate in their value over time and require active administration. Real estate, on the other hand tends to retain its value better that other assets like gold or mutual funds.

It comes down to choosing something that is right for you. The key to choosing the right investment is knowing your risk tolerance, how much income you require, and what your investment objectives are.

Once you've decided on what type of asset you would like to invest in, you can move forward and talk to a financial planner or wealth manager about choosing the right one for you.

Why it is important that you manage your wealth

The first step toward financial freedom is to take control of your money. Understanding your money's worth, its cost, and where it goes is the first step to financial freedom.

You also need to know if you are saving enough for retirement, paying debts, and building an emergency fund.

If you do not follow this advice, you might end up spending all your savings for unplanned expenses such unexpected medical bills and car repair costs.

How do I start Wealth Management?

The first step towards getting started with Wealth Management is deciding what type of service you want. There are many types of Wealth Management services out there, but most people fall into one of three categories:

-

Investment Advisory Services: These professionals can help you decide how much and where you should invest it. They provide advice on asset allocation, portfolio creation, and other investment strategies.

-

Financial Planning Services: This professional will work closely with you to develop a comprehensive financial plan. It will take into consideration your goals, objectives and personal circumstances. They may recommend certain investments based upon their experience and expertise.

-

Estate Planning Services- An experienced lawyer will help you determine the best way for you and your loved to avoid potential problems after your death.

-

Ensure that the professional you are hiring is registered with FINRA. You can find another person who is more comfortable working with them if they aren't.

Statistics

- A recent survey of financial advisors finds the median advisory fee (up to $1 million AUM) is just around 1%.1 (investopedia.com)

- US resident who opens a new IBKR Pro individual or joint account receives a 0.25% rate reduction on margin loans. (nerdwallet.com)

- As of 2020, it is estimated that the wealth management industry had an AUM of upwards of $112 trillion globally. (investopedia.com)

- If you are working with a private firm owned by an advisor, any advisory fees (generally around 1%) would go to the advisor. (nerdwallet.com)

External Links

How To

How to Beat the Inflation by Investing

Inflation is one factor that can have a significant impact on your financial security. Inflation has been steadily rising over the last few decades. Different countries have different rates of inflation. India is currently experiencing an inflation rate that is much higher than China. This means that even though you may have saved money, your future income might not be sufficient. You may lose income opportunities if your investments are not made regularly. So, how can you combat inflation?

Investing in stocks is one way to beat inflation. Stocks can offer a high return on your investment (ROI). These funds can also help you buy gold, real estate and other assets that promise a higher return on investment. There are some things to consider before you decide to invest in stocks.

First, decide which stock market you would like to be a part of. Are you more comfortable with small-cap or large-cap stocks? Choose according. Next, understand the nature of the stock market you are entering. Are you looking for growth stocks or values stocks? Decide accordingly. Finally, you need to understand the risks associated the type of stockmarket you choose. There are many kinds of stocks in today's stock market. Some stocks can be risky and others more secure. Make wise choices.

If you are planning to invest in the stock market, make sure you take advice from experts. They will be able to tell you if you have made the right decision. You should diversify your portfolio if you intend to invest in the stock market. Diversifying increases your chances of earning a decent profit. You risk losing everything if only one company invests in your portfolio.

You can consult a financial advisor if you need further assistance. These professionals will assist you in the stock investing process. They will make sure you pick the right stock. You will be able to get help from them regarding when to exit, depending on what your goals are.